Ben Watts · REA Spring Forum · 7 May 2026 ben@kilowatts.io · linkedin.com/in/kilowatts

Slides live: reaspring2026.kilowatts.io

reaspring2026.kilowatts.io

Scan the QR — or go to slido.com and enter the event code

slido.com

Word cloud, polls and live Q&A throughout. First question coming up…

1. A solar MW in the UK now earns more than one in Spain — what just happened to solar economics across Europe.

2. Good or bad neighbours? Cui bono? — what GB's interconnector flows reveal about who's paying for the transition.

The thread: continental cannibalisation flows across borders, and Britain sits at the crossroads.

A British solar MW now out-earns a Spanish one — despite half the sunshine.

Spain used to earn ~2× the UK. The lines crossed in 2025.

Spain has ~2× the yield. UK has ~2× the capture price. Net winner: UK.

Sunnier countries earn less per MWh. The cannibalisation gradient runs south to north.

Spain went from ~30% of summer-peak demand in 2021 to ~100% by 2025. Britain's build was much slower.

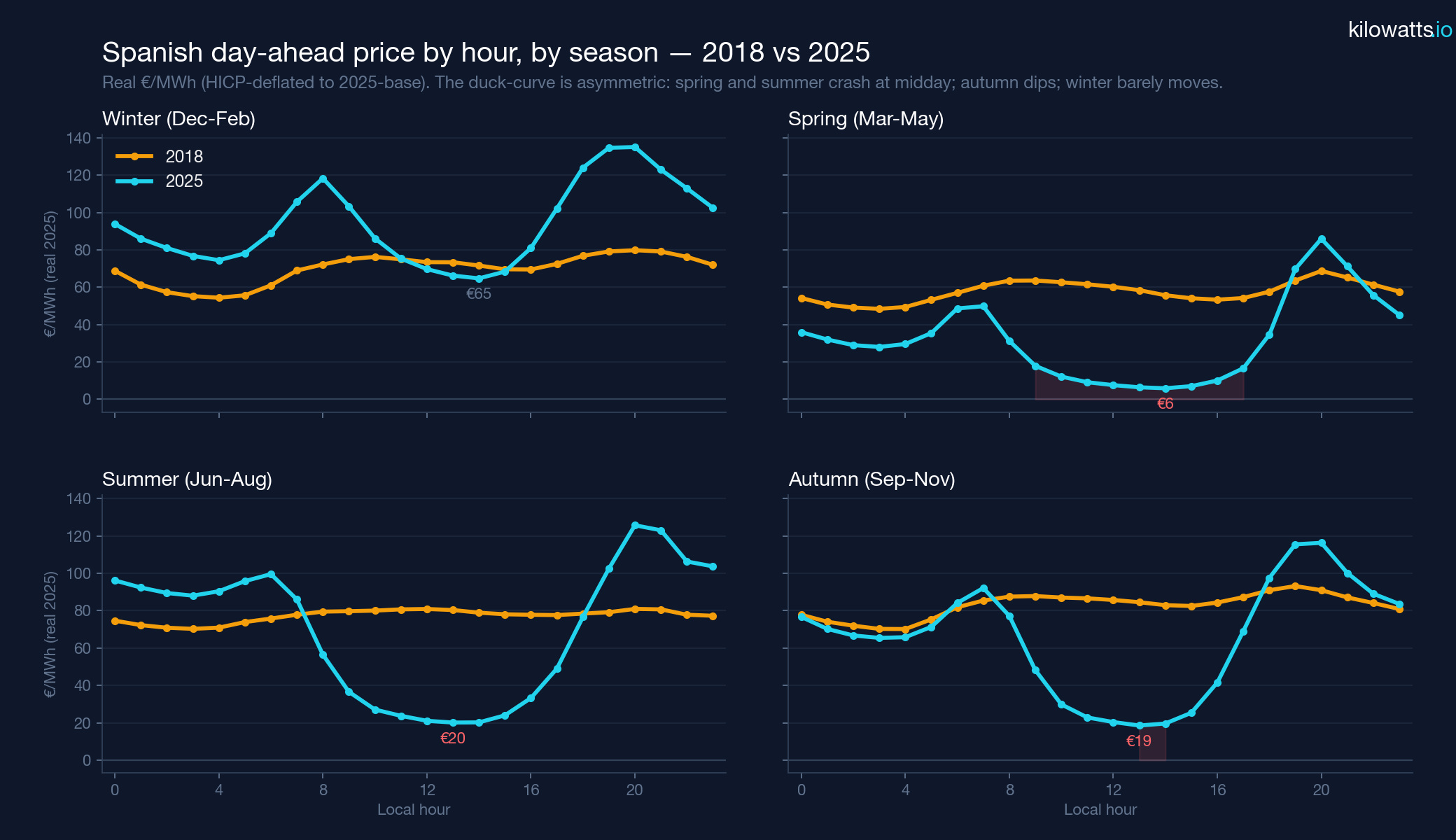

In 2018, prices were flat (gas-led). By 2025, a deep solar trough year-round. Winter now out-earns spring for Spanish PV.

Cannibalisation hits spring midday hardest; winter dodges it. Hot summer evenings (AC + late dinner) earn more than midday.

Continued Spanish capacity additions + gas-volatility tailwind for GB → the crossover is structural, not a one-off.

A solar MW in the UK now earns more than one in Spain

dispatches.kilowatts.io/p/a-solar-mw-in-the-uk-now-earns-more

Hydro to the north · sun to the east · datacentres to the west · nukes to the south. Different and unexpected trends in every direction.

A picture tells a thousand words; this animation tells a thousand pictures.

NSL = highest buy-low / sell-high spread of any GB IC. The big Nordic battery delivers.

Even Norway has bad quarters. Climate-change-induced droughts will recur — being a good neighbour back matters.

GB used to import all day from the continent. Now, in summer, we import the duck — and export at sunset.

Continental ICs lower midday residual by ~2 GW (good) but add ~2.4 GW to GB's evening ramp window (50% harder for the GB system to follow).

The 30-year IFA story. Only really asked GB for help once: 2022, when nuclear collapsed at the worst possible time.

Wind surplus → datacentre baseload deficit. GB CCGT often the marginal generator for Irish AI.

GB has paid more for carbon than the EU every year since 2018. ~£23/MWh added to GB CCGT SRMC at today's price.

When ICs over-earn, GB consumers get money back via reduced TNUoS. The red wedge is the rebate.

Good or bad neighbours? Cui bono (who pays)?

dispatches.kilowatts.io/p/good-or-bad-neighbours-cui-bono-who